Recent OECD-FAO Agricultural Outlook reports have focused on high and volatile agricultural commodity prices, stressing that prices would come down as markets respond but would remain on a higher plateau underpinned by continuing strong demand and rising costs for some inputs. As anticipated, prices have started to ease but remain at relatively high levels. Food price inflation at the retail level has fallen significantly from its peak in 2008 and its contribution to overall inflation has moderated. Nevertheless, food price inflation remains high in many developing countries and is still outpacing overall inflation in the majority of countries examined.

Price volatility remains a concern, with weather-related yield variability the main threat as long as stocks remain low. With a rebound in crop production, stocks have improved somewhat and markets in 2012 appear less turbulent. The key issue facing global agriculture is how to increase productivity in a more sustainable way to meet the rising demand for food, feed, fuel. and fibre.

Nominal prices of the commodities covered in this Outlook are expected to trend upwards over the next 10 years (see Figure 1) and are projected to average 10%-30% above those of the previous decade. Prices in real terms (adjusted for inflation) will remain flat or decline from current levels. Global agriculture is increasingly linked to energy markets (see Figure 5). Oil price projections contained in the macroeconomic assumptions are on average about USD 25 above those used last year (ranging from USD 110 to USD 140 per barrel over the Outlook period). These higher oil prices are a fundamental factor behind the higher agricultural commodity price projections, affecting not only oil-related costs of production but also increasing the demand for biofuels and the agricultural feedstocks used in their production.

Despite strong prices, slower production growth is anticipated. Growth in global agricultural production has been above 2% p.a. over the past several decades, but is projected to slow to 1.7% p.a. over the next decade (see Figure 2). Growing resource constraints, environmental pressures, and higher costs for some inputs are anticipated to inhibit supply response in virtually all regions. In this context, this Outlook suggests that more attention be paid to increasing sustainable agricultural productivity growth.

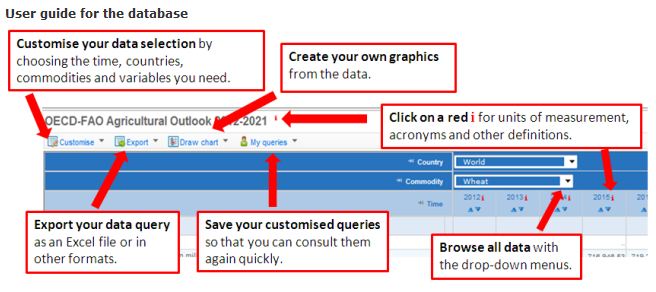

You can browse the OECD-FAO Agricultural Outlook database in English or French using 3 basic queries sorted by commodity (i.e. agricultural product), country (including regions e.g. European Union) and variable (e.g. production, price, consumption, import, export).